How to Know If You Have a Good Credit Score (and How to Improve It)

18 Jul How to Know If You Have a Good Credit Score (and How to Improve It)

Posted at 12:36h in

A Good Credit Score isn’t as easy to pin down as it may seem. Learn how to tell whether you have a good credit score and what you can do to improve it!

How do you know if you really have a good credit score? This is more confusing than it may seem. There are multiple credit scoring models and each one is different. So the same number might be great in one model and average in another!

Furthermore, every creditor and lender uses different scores! This is due to the differences in their purpose—home loans vs credit cards, for instance—as well as differences in their lending policies.

So no one but the lender knows which score they’ll use and how they’ll look at it. But there are a few facts and guidelines you can learn. These can help you predict whether yours will be generally considered a good credit score.

So… Many… Credit Scores!

The real difficulty is in the variety of credit score models. Each one has its own range of credit scores. Obviously, the first thing you need to know is which range of scores you’re dealing with.

There are many credit reporting agencies with their own scoring models. However, there are six that dominate the market, each with their own range of scores:

- FICO Score: 300-850.

- VantageScore 3.0: 300–850.

- VantageScore 1.0 and 2.0: 501–990.

- Experian PLUS Score: 330-830.

- TransUnion New Account Score 2.0 (formerly TransRisk score): 300-850.

- Equifax Credit Score: 280–850.

As you can see, what’s considered a “good credit score” really depends on the model. An 840 FICO score is just 10 points below “perfect”. That’s almost unheard of and would be rated as “super-prime.” However, in the VantageScore 2.0 model, 840 is 150 points from “perfect”.

If that weren’t complicated enough, one must also consider the lenders, themselves! Even if they use the same credit score, every lender is still unique and may evaluate that credit score differently.

One lender might only approve applicants with a credit score over 750, while the other might go as low as 680. Additionally, even when two lenders use the same credit score and both approve applicants below 700, one will likely charge higher interest than the other!

There’s plenty here to cause the average person to feel overwhelmed. But don’t give up hope just yet! Like all bodies of knowledge, there are a few tricks that can help.

Understanding Various Credit Scores

The key to knowing whether you have a good credit score is knowing what your creditor is using it for. Let’s say you called your credit card company to ask for a better interest rate. It might go with TransUnion New Account Score 2.0, which TransUnion especially designed “to help institutions … identify the most profitable existing accountholders.”

Another creditor might use the much more common and general FICO score or VantageScore 3.0. What do all three of those credit scoring models have in common? They all use a range of 300-850!

Again, different models used for different purposes are going to have different results. That said, predicting what will probably be considered a good credit score in general is fairly safe. Especially since the most commonly used scores have the same range.

How credit scores are evaluated in models with a range of about 300 to about 850 generally looks like this:

- “Excellent” = 750 or above

- “Good” = 700-749

- “Fair” or “Average” = 650-699

- “Poor” = 600-649

- “Bad” = 600 or below

How to Build and Keep a Good Credit Score

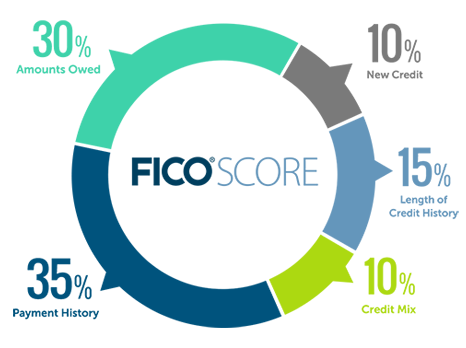

Being able to tell if you have a good credit score in general is one thing. Understanding what makes a credit score good or bad is if anything more important! The good news there is that credit score models are largely based similar criteria:

- Payment History

- Credit Utilization

- Length of Credit History

- Mix of Accounts

- New Credit Inquiries

Individual accounts may have very different impacts on your score depending on the model. Still, most generally use a formula similar to FICO’s. (See image.)

So what does all of that mean and what can you do? There are lots of answers to those questions, and it depends on your specific situation. However, there are some quick tips you can follow:

- Payment History: Make your loan payments on time. The fewer late payments in your history, the better!

- Credit Utilization: Keep your total debt below 30% of your total credit limits. Those with the highest scores are typically only using about 10% or less of their available credit, spread out across all of their accounts.

- Length of Credit History: Maintain your credit accounts. Keep them open and active! Years of timely payments establishes your reputation as a good lendee.

- Mix of Accounts: Who would you loan to first? Someone with three credit cards in their history, two of which are recent? Or someone else with more than a decade of paying their mortgage, car loan, and a variety of credit?

- New Credit Inquiries: This is especially important before applying for a loan. If you apply for new credit several times in the year prior, it indicates you’ve been “shopping around” and may have spread yourself too thin. That’s risky behavior in a lender’s eyes.

- How can you tell if your credit is staying where it should be? Sign up for credit monitoring! This is also an essential way of knowing whether inaccurate accounts are wrecking your credit. Keep careful watch of your monthly credit scores to find out if your credit-building and maintenance strategy is working.

Conclusion:

No blog post can give you suggestions specific to your financial situation. That takes a qualified credit expert. But implementing the above can help significantly. And now you’re better equipped for when you apply for new credit or a loan!

You know what ingredients make up a good credit score, the differences between the various credit score models, and what you can do right now to make a difference.

For more specific ways, detailed ways you can improve your credit, be sure to download our free guide: 3 Hot Tips to Improve Your Credit!

Have questions or want to share your story right now? Comment below!